kampanye Trump mirip kampanye Farage... sesaat setelah sadar ia menang, Farage berubah pikiran seketika, karna amat sadar konsekuensi ekonominya AMAT PARAH bwat INGGRIS (tanpa Skotlandia, n kemungkinan disusul tanpa Irlandia Utara)

... tampaknya TRUMP TIDAK PEDULI ... Trump triumph ... tapi seketika terpilih, seketika itu juga BERUBAH LAH CARA BICARA TRUMP ... gejala awal terjadinya PERUBAHAN MENDASAR bahwa TRUMP KEMUNGKINAN BESAR akan MENAKAR KEMBALI janji2 kampanyenya, termasuk yang EKSTREM KANAN (white only politics)

Republicans claim that when the FBI got a secret court order to spy on former Trump campaign adviser Carter Page during the election, it relied “extensively” on information from a politically motivated British ex-spy who was being funded by Democrats to find dirt on Donald Trump. And it didn't share those political motivations with a secret court that ultimately authorized the surveillance. That's the gist of the declassified memo written by House Republicans, which President Trump agreed Friday to release despite concerns from the FBI and Justice Department that the memo is inaccurate and risks undermining source-gathering methods and ongoing investigations. Here's a quick breakdown of the allegations in the memo and the outstanding questions surrounding it: 1. The dossier funded by Democrats formed “an essential part” of the FBI's application to spy on Trump campaign adviser Carter Page.

Getting a secret court to approve spying on an American citizen is no small thing. It requires an application that former FBI director James B. Comey has said is “thicker than my wrists.” Former FBI agent Asha Rangappa told The Fix that a Foreign Intelligence Surveillance Act application (referred to as “FISA application” in the memo) probably involved a dozen people's insights and intelligence. This memo alleges the dossier put together by Christopher Steele was “an essential part” of that application. Page had been on the FBI's radar at least since 2013, so it would be remarkable if the dossier, which was shared with the FBI in late 2016, was the essential piece of information used for the application. Outstanding questions: Given that this seems to be the key point of the memo — the FBI relying on a politically motivated document to spy on a U.S. citizen — its description of how important the Steele memo was to the FBI's surveillance of Page is vague. How much constitutes “an essential” part of the application? The FBI officials have told my Post colleagues that the memo was far from the only piece of intel it used to get court permission to spy on Page. 2. Senior Justice Department and FBI officials knew Democrats were funding this research but didn't tell the court of the party's role.

When BuzzFeed published this dossier in January 2017, we didn't know who funded Steele's work. We now know Democrats were, indirectly. A conservative publication hired the opposition research group Fusion GPS to get dirt on Trump during the GOP primaries. After Trump won the Republican presidential nomination, the Democratic National Committee and Hillary Clinton's presidential campaign started paying Fusion GPS to continue the research. That's when Fusion GPS hired Steele. This memo alleges that the FBI and top Justice Department officials knew Democrats were funding the dossier but did not share that with the court that approved the original surveillance order or any of the four renewals. (A surveillance order must be renewed every 90 days, with FBI officials having to convince federal judges the warrant is yielding legitimate information relevant to the FBI’s case.) Outstanding questions: Does who funded dossier really matter to the court? The company behind the dossier testified to Congress that Steele’s report isn’t fake, was not politically motivated and did not set out with the intention to smear Trump, least of all to find collusion. 3. The FBI should have terminated a contract with Steele after he spoke with the media.

The rest of the memo attempts to provide corollary evidence that Steele was not a reliable source for the FBI. Here, House Republicans argue that the FBI hired Steele during the campaign as one of its informants and then didn't let him go after he talked to the media — including for a September Yahoo News article. The FBI cut him off only after he disclosed his relationship with the FBI in an Oct. 30 Mother Jones article. The memo also alleges Steele lied to the FBI about talking to Yahoo News and other media outlets more than a month earlier, ostensibly to keep his job: “Steele improperly concealed from and lied to the FBI about those contacts,” the memo reads. More: Steele's numerous encounters with the media violated the cardinal rule of source handling — maintaining confidentiality — and demonstrated that Steele had become a less than reliable source for the FBI. Outstanding question: It's not immediately clear how this affects the information that made its way into the FISA warrant. 4. Steele had his own political bias that the FBI “ignored or concealed.”

Here's another reason Steele's information can't be trusted, House Republicans allege: He had it in for Trump. The memo alleges that Steele told a top Justice Department official he “was desperate that Donald Trump not get elected and was passionate about him not being president.” The memo says that the Justice Department official told the FBI of the “clear evidence of Steele's bias,” but it was “not reflected in any of the Page FISA applications.” Outstanding questions: It's an open question whether Steele's bias matters if the information he provided was sound. Talking about how the FBI got the information is a distraction from what agents found, Jens David Ohlin, a dean at Cornell Law University, told The Fix earlier this week: “Consider an analogy. Say there’s a murder in a small town, and the police aren’t making any progress. In frustration, the family of the victim hires a private investigator who turns up evidence and gives it to the police. What should the police do? Answer: They should act on it if there’s something there.” 5. At least two FBI officials had a clear bias against Trump.

At the very end of the memo, its authors also mention FBI officials Peter Strzok and Lisa Page, who were having an affair and texted frequently about the investigation, including exchanging pro-Clinton texts and expressing anti-Trump sentiments. This memo also alleges the FBI needlessly mentioned former Trump foreign policy adviser George Papadopoulos in its application to spy on Page. Papadopoulos later pleaded guilty to lying to the FBI about his conversations with Russians during the campaign. Outstanding question: Unless House Republicans are alleging the entire FBI was biased against Trump, it's not clear how this affects the FISA application that ultimately let the FBI spy on Page. Strzok was a key member of the team investigating Russian interference in the 2016 election, but he was reassigned after the FBI discovered these texts. Also, the memo arguably undercuts itself when it acknowledges that Papadopoulos was what triggered the FBI investigation, not the Steele dossier. 6. Republicans released this memo because “the public interest in disclosure outweighs any need to protect the information.”

Legal experts, Democrats, intelligence officials and some Republican members of Congress have heavily criticized this memo as needlessly declassifying information to prove a political point. The process this memo went through to get released is highly unusual, former congressional staffers say. The White House pushes back on that characterization by saying “the public interest in disclosure outweighs any need to protect the information.” White House lawyer Donald McGahan wrote that in a letter attached to the memo. Outstanding question: The memo has yet to answer why Trump's handpicked head of the FBI disagrees.

🐉

THE NATION: Asked at the close of the Constitutional Convention of 1787 if the delegates had created a republic or a monarchy, Benjamin Franklin is reported to have replied: “A republic, if you can keep it.”

Paul Ryan has abandoned the effort to keep it.

At the heart of the US Constitution is a system of checks and balances that was established primarily to guard against the concentration of power in an executive branch that might tend toward royalism. The founders of the American experiment wanted to prevent a repeat of the monarchical abuses of King George III, against which their constituents had risen in revolution.

“The accumulation of all powers, legislative, executive, and judiciary, in the same hands, whether of one, a few, or many, and whether hereditary, selfappointed, or elective, may justly be pronounced the very definition of tyranny,” warned James Madison, the essential author of the Constitution, who explained, “The great security against a gradual concentration of the several powers in the same department, consists in giving to those who administer each department the necessary constitutional means and personal motives to resist encroachments of the others.”

What Madison asserted in the late 1780s remains true to this day: For the system of checks and balances to function, the leaders charged with responsibility for the various branches of government must zealously defend the authority of the branches they lead. They cannot allow one branch to become the extension of another.

This is the basic duty that House Speaker Paul Ryan rejected when he chose to make the legislative chamber subservient to President Trump’s lawless executive branch. Ryan’s abandonment of the Constitution began long ago. But it culminated with the speaker’s decision to support Friday’s release of a partisan memo produced by disgraced House Permanent Select Committee on Intelligence chair Devin Nunes (R-CA) to discredit law-enforcement agencies that have organized and supported inquiries into Trump campaign and Trump administration wrongdoing.

“Discrediting law enforcement is the memo’s transparent purpose and why it has been embraced by President Trump,” argued a Washington Post editorial that condemned Ryan’s choice. “Written mainly by the staff of Devin Nunes (R-CA), the loose-cannon chairman of the House Permanent Select Committee on Intelligence, the memo reportedly makes the case that the FBI abused spying authorities as it sought permission to surveil a former Trump adviser,” noted the Post. “The Justice Department called its potential release, which Mr. Trump reportedly intends to approve, ‘extraordinarily reckless.’ The FBI released its own startling public statement citing ‘grave concerns about material omissions of fact that fundamentally impact the memo’s accuracy.’ Adam Schiff (D-CA), the ranking Democrat on the Intelligence Committee, wrote in a Post op-ed that the Nunes memo ‘cherry-picks facts, ignores others and smears the FBI and the Justice Department.’”

The Post’s editorial appeared just before the release of the memo. But the concerns it expressed were confirmed by the document, which makes over-the-top and highly speculative allegations about how the inquiry into the Trump team’s Russia ties has been conducted, and especially about how FISA warrants were obtained, but fails to present an even minimally credible case that the inquiry is unnecessary or inappropriate.

That memo is so thin in content and character that it adds weight to the argument made by the Post with a headline that read: “Paul Ryan is tarnishing the House.”

The speaker’s embrace of Nunes and his memo has dishonored the chamber that he, above all others, is duty bound to defend.

But that is the least of the sins against the American experiment committed by Ryan in collaboration with Nunes. Illinois Congressman Mike Quigley, a key Democrat on the Intelligence Committee, aptly describes Ryan and Nunes as “co-conspirators” in doing the bidding of a president who has “freaked out” over special counsel Robert Mueller’s investigation into Russian meddling in the 2016 presidential election.

Nunes is a secondary figure, whom Quigley appropriately dismisses as nothing more than an agent for Trump.

Ryan’s dereliction of duty is the more serious matter, as it betrays the most fundamental tenets of the Constitution. When the speaker chose to facilitate this bungling effort by Nunes to smear the Federal Bureau of Investigation and the Department of Justice on Trump’s behalf, the Wisconsin Republican signaled a willingness to make the House of Representatives an appendage of the White House.

In so doing, Ryan abandoned the solemn oath he swore “to support and defend the Constitution of the United States against all enemies, foreign and domestic…”

Paul Ryan is not supporting the Constitution. He is shredding it. It is grotesque for the speaker to claim that he is aiding and abetting Nunes because “that brings us accountability, that brings us transparency, that helps us clean up any problem we have with [the Justice Department] and FBI”—as Ryan did Thursday in a crudely defensive and wildly dishonest attempt to deny his true intentions.

Make no mistake: Paul Ryan has zero interest in accountability, transparency or cleaning up problems with law-enforcement agencies and the investigative process. He has shown no interest in legitimate and necessary oversight of intelligence agencies. He has never been identified with the cause of civil liberties or with the defense of privacy rights.

What Paul Ryan has been identified with is extreme partisanship and with the determination of congressional Republicans to defend Donald Trump—even if that defense comes at the cost of a system of checks and balances that was established 231 years ago to guard against precisely the abuses that are now occurring.

John Nichols is The Nation’s national-affairs correspondent. He is the author of Horsemen of the Trumpocalypse: A Field Guide to the Most Dangerous People in America, from Nation Books, and co-author, with Robert W. McChesney, of People Get Ready: The Fight Against a Jobless Economy and a Citizenless Democracy.

🍚

marketwatch: Alan Greenspan, who warned of “irrational exuberance” during the dot-com bubble of the 1990s, said Wednesday that Wall Street is in another bubble. Two, in fact.

“There are two bubbles: We have a stock market bubble, and we have a bond market bubble.”

“At the end of the day, the bond market bubble will eventually be the critical issue,” the former Fed chairman said in an interview with Bloomberg TV.

“For the short term it’s not too bad,” Greenspan said. “But we’re working, obviously, toward a major increase in long-term interest rates, and that has a very important impact, as you know, on the whole structure of the economy.”

Greenspan, who led the Fed from 1987 to 2006, cited the growing federal deficit as the reason behind the bond bubble, and said he worries that raising interest rates too quickly will fuel inflation.

“We are dealing with a fiscally unstable long-term outlook in which inflation will take hold,” he said. “In fact I was very much surprised that in the State of the Union message yesterday all those new initiatives were not funded and I think we’re getting to the point now where the breakout is going to be on the inflation upside. The only question is when.”

Add meager productivity growth and a falling dollar, and “we are working our way towards stagflation,” he said.

Earlier Wednesday, the Fed said it expected inflation to rise to about 2% this year, hinting that it will likely raise interest rates at its next meeting in March.

🍓

post-gazette: During my morning run last Thursday, I couldn’t get out of my mind the image of Donald Trump and the Republican Congress members standing outside Wednesday in their thousand-dollar suits and thousand-dollar ties, with their thousand-dollar smiles — glad-handing and applauding one another for their passage of a tax reform bill.

They all seemed to feel so good about themselves and the tremendous accomplishment they had just achieved for the American people, some even emboldened enough to speculate on what they would “fix” next — Social Security, the Affordable Care Act, welfare reform, any or all of the so-called entitlement programs that could use their magic touch that was so deftly applied to our tax laws.

However, it is an absolute disgrace that while the president and the Republican Congress are congratulating themselves in Washington, historic fires continue to burn in California, tens of thousands of our fellow citizens in Puerto Rico are still without power, people in Houston and Florida are still living in tents following epic hurricanes, and the average life expectancy of our citizens declined for the second year in a row, due primarily to the opioid crisis. All of Congress is apparently too preoccupied with tax reform to address life-and-death struggles of their constituents.

Time will tell if the tax reform legislation passed last week will be the catalyst for unprecedented prosperity for the middle class, but in the interim, can our dysfunctional government please come together to address the myriad of humanitarian crises that continue to plague the good citizens of this great country?

DAVID HOLLIFIELD

Findlay

🌵

Kabar24.com, JAKARTA - Industri majalah dewasa melambungkan Hugh Hefner di dunia. Ia disebut-sebut membantu mengantarkan revolusi seksual tahun 1960-an dengan majalah pria yang inovatif dalam hal melangkahi tabu, terutama di dunia timur.

Hefner membangun kerajaan bisnis di seputar gaya hidupnya yang libert, dan akhirnya meninggal, Rabu pada usia 91 tahun.

Keterangan kematian Hefner itu disampaikan pihak Playboy Enterprises.

Hefner, yang pernah disebut "nabi hedonisme pop" oleh majalah Time, meninggal dengan damai di rumahnya, Playboy Enterprises mengatakan dalam sebuah pernyataan.

Hefner kadang-kadang disebut sebagai Pan Peter yang terlalu banyak waktu. Dia menyimpan 7 harem berambut pirang muda di Mansion Playboy legendarisnya.

Hal itu dicatat dalam "The Girls Next Door," sebuah reality show TV yang ditayangkan mulai tahun 2005 sampai 2010.

Dia mengatakan bahwa berkat obat penghambat impotensi Viagra dia terus menjalankan libido ke usia 80-an.

"Saya tidak akan pernah tua," kata Hefner dalam sebuah wawancara CNN saat berusia 82 tahun.

"Tetap muda adalah apa adanya bagi saya. Berpegang pada anak laki-laki itu dan lama sekali saya memutuskan bahwa usia benar-benar tidak masalah dan selama para wanita ... merasakan hal yang sama, tidak masalah dengan saya, " ujarnya.

Hefner agak telat saat menjadikan Crystal Harris, yang berusia 60 tahun lebih muda, sebagai istri ketiganya pada tahun 2012. Saat itu Hefner telah berusia 86 tahun.

Dia mengatakan bahwa gaya hidupnya mungkin merupakan reaksi atas kehidupannya di tengah keluarga yang tertekan dan jarang merasakan kasih sayang.

Masa kecilnya yang tak menyenangkan menyebabkan perusahaan multijuta dolar Hefner berpusat pada wanita telanjang sekaligus mendukung filosofi Playboy Hefner atas romantisme, gaya dan ikatan adat istiadat.

Filosofi itu mewujud di pesta-pesta legendaris di rumah-rumah mewahnya - pertama di kampung asalnya Chicago, kemudian di lingkungan eksklusif Holmby Hills di Los Angeles - tempat serombongan selebriti pria berkerumun untuk bergaul dengan para wanita muda cantik.

Sumber : Reuters

👹

marketwatch: As the Federal Reserve prepares to begin paring the size of its $4.5 trillion balance sheet next month, analysts at Deutsche Bank this week warned that what they have dubbed the “great central bank unwind” is one of several candidates for creating the next financial crisis.

“When looking for the next financial crisis, it’s hard to escape from the fact that we’re seemingly in the early stages of the ‘great unwind’ of global monetary stimulus at the same time as global debt remains at all-time highs following an increase over the past decade—at the government level at least—which has been unparalleled in peacetime history,” wrote strategists led by Jim Reid in an 88-page study entitled, “The Next Financial Crisis.”

The wide-ranging report examines other potential sparks for the next financial cataclysm, including political turmoil in Italy, a potential “China crisis,” the rise of populism and the impact of Britain’s formal exit from the European Union.

As for the unwind, the Fed, as expected, formally announced it would begin the slow wind-down of its balance sheet in October. The balance sheet grew to gigantic proportions as a result of an aggressive asset-buying program designed to push down long-term interest rates, push investors into riskier assets, spur investment and underpin a then-crisis-stricken economy.

The Fed ended its bond-buying in 2014, but maintained the size of its balance sheet by reinvesting proceeds as Treasurys and mortgage-backed securities matured. Now, the Fed is prepared to slowly let those assets work themselves off the balance sheet—a prospect that has done little to unsettle the markets.

But the Deutsche Bank strategists wondered if investors have simply become blasé about the size of central-bank balance sheets and the scope of the effective money printing the so-called quantitative-easing programs have entailed. The ECB continues to add assets to its balance sheet, a process that is expected to downshift next year. The Bank of Japan is also engaged in extraordinary stimulus efforts and the Bank of England maintains a hefty asset portfolio as a result of its own earlier QE initiative.

“You slowly become anchored to believe the current situation is normal as it’s persisted for so long now,” they wrote. “However it’s anything but normal. Since the financial crisis, $10 trillion plus has been added to the balance sheets of the four largest central banks with over $14 trillion of assets now owned.”

The analysts pointed to the charts below, showing the real adjusted balance-sheet size of the four largest developed market central banks through history.

The analysts argue that it’s more than a monetary phenomenon. Throwing in the cumulative government budget deficits of the U.S., U.K., Japan and the eurozone since the 2008, they come up with total combined QE and fiscal-stimulus sum of $34 trillion.

“In the end, $34 trillion of stimulus and QE has delivered only very low growth, subdued inflation and sky-high asset prices around the globe,” they wrote. “This is unprecedented territory and how can anyone estimate what the fallout will be when we normalize again?”

Indeed, Fed skeptics question how central banks can undo stimulus without creating headwinds for financial markets. If the goal of QE was to drive up bond prices and drive down long-term yields, why wouldn’t an unwind put upward pressure on yields. Bond prices and yields move in opposite directions. Observers who believe that low yields offered investors desperate for returns no choice but to pile into stocks and other assets perceived as risky wonder whether the market is due for a comeuppance.

They argue that the rise in global equities, which has seen the S&P 500 SPX, -0.14%advance around 270% over the course of the bull market that began in 2009, can be attributed in part to QE.

Others question whether QE had a lasting effect on yields and asset prices. They argue that the bulk of the gains in the stock market in recent years can be attributed to low interest rates, slow but steady growth and strong corporate profits. Also, the size of the balance sheet has shrunk relative to the economy and total debt.

The Deutsche Bank strategists, meanwhile, argue that aggressive money printing by major central banks has “obviously” been a response to the huge rise in the debt burden since the financial crisis. Government debt has continued to climb but yields have fallen due to QE.

As a result, the ratio of Group of Seven government debt to gross domestic product is now at a peacetime peak, while interest rates within the past year have hit multi-century, all-time lows. In fact, both base rates and long-term yields across a swath of the world have fallen into negative territory.

The strategists argue that when thinking about the possible causes of the next financial crisis, it would pay to consider “that we are at a unique point in time with regards to the relationship between debt, interest rates and central bank balance sheets,” they wrote.

That means the unwind of QE is a “journey into the unknown and history would suggest there will be substantial consequences of the move especially given the elevated level of many global asset prices,” the strategists said.

Even if the unwind stalls or the economy unexpectedly weakens “we will still be left with an unprecedented global situation and one which makes finance inherently unstable even if we are currently living in the lowest volatility markets on record.”

This article was originally published on Sept. 20.

💣

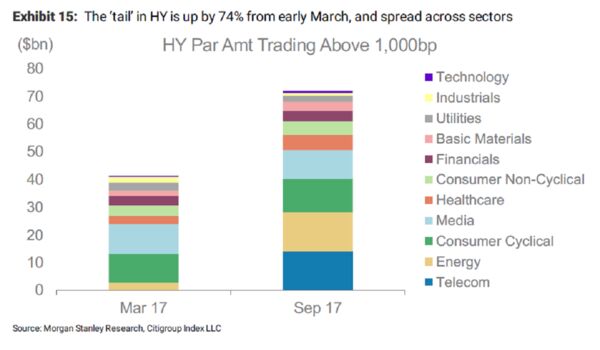

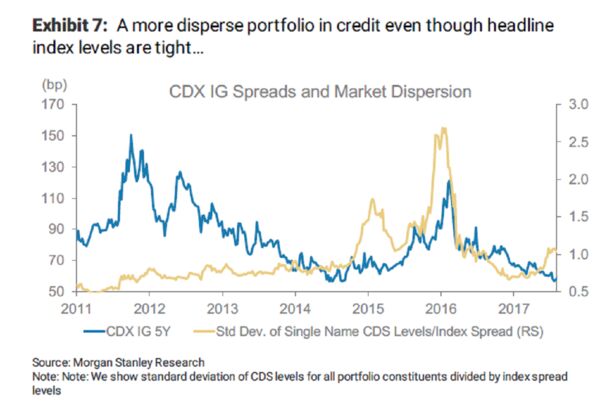

bloomberg: Beneath the tranquil surface of U.S. credit markets, bearish winds are blowing. Issuer and sector-specific risks are increasing while the pile of debt trading at distressed levels is rising -- evidence the post-crisis debt bull-run is peaking.

That’s the alarm sounded by Wall Street arch-bears Morgan Stanley after a deep dive into the shifting credit landscape in recent months, which they reckon vindicates a long-standing call that junk premiums aren’t compensating investors for the risks.

One warning sign: The face-value of high-yield debt trading at distressed levels has risen by about $30 billion from March to mid-September.

Morgan Stanley

Another: The dispersion between credit spreads -- the degree to which bonds are priced according to issuer and sector-specific risks -- is slowly rising. That underscores increasing credit concerns that are masked at the index level, as cheap liquidity and low volatility cap risk premiums for companies with stronger balance sheets, according to Morgan Stanley.

Morgan Stanley

Money managers are grappling with an uptick in operational and balance-sheet challenges late in the business cycle, with debt-laden Toys ’R Us Inc. the latest retailer to file for bankruptcy this week, catching bond markets off guard.

"Companies with the weakest fundamentals often show problems first late in a cycle, and the retail sector has many such examples," said Adam Richmond, Morgan Stanley’s chief credit strategist.

"Investors initially treat those issues as idiosyncratic, and then the problems spread, when credit conditions begin to tighten,” he said. “That is how the late cycle can transition to end of cycle."

These risks are hard to see at the index level, with the Bloomberg Barclays U.S. high-yield benchmark up almost 7 percent this year, led by CCC-rated names. Still, the latter has underperformed the broader market over the past two months, suggesting investors are increasingly compelled to price-in deteriorating fundamentals -- reminiscent of a market in its late winter, according to the U.S. lender.

Some 119 speculative-grade U.S. bonds currently trade below 80 cents on the dollar -- one rough rule of thumb to denote distressed junk names -- compared with 23 obligations in early March, according to Bloomberg data.

"Dispersion in 2015 and 2016 was higher in-line with markets that were more volatile as well there being a strong sectoral component to the selloff, i.e. commodity-sensitive sectors," wrote Vishwas Patkar, credit analyst at the U.S. bank. "This time around, it is notable that we are seeing dispersion rise even though spread levels are very tight -- and there isn’t really a one sector story."

Tighter financial conditions will eventually pave the way for higher defaults and wider spreads, suggesting investors should favor higher-quality companies, the bank concludes.

"The market is penalizing weak companies across different sectors,” Patkar added. "This is, we believe, yet another late-cycle indicator."

👻

By Kimberly Amadeo

Updated September 18, 2017

Definition: The debt ceiling is a limit that Congress imposes on how much debt the federal government can carry at any given time. When the ceiling is reached, the U.S. Treasury Department cannot issue any more Treasury bills, bonds or notes. It can only pay bills as it receives tax revenues. If the revenue isn't enough, the Treasury Secretary must choose between paying federal employee salaries, Social Security benefits or the interest on the national debt.

The nation's debt limit is similar to the limit your credit card company places on your spending. But there's one significant difference. Congress is in charge of both its spending and the debt limit. It already knows how much it will add to the debt when it approves that year's budget deficit. When it refuses increase the debt limit, it's saying it wants to spend but not pay its bills. That's like your credit card company allowing you to spend above its limit and then refusing to pay the stores for your purchases.

Congress imposes the debt ceiling on the statutory debt limit. That's the outstanding debt in U.S. Treasury notes after adjustments. The adjustments include unamortized discounts, old debt and guaranteed debt. It also includes debt held by the Federal Financing Bank. The statutory debt limit is just a little less than the total outstanding U.S. debt recorded by the national debt clock.

The U.S. debt consists of two types of debt. The first is what the government owes to itself. Most of that is the Social Security Trust Fund and federal employee retirement funds.The debt that's owed to everyone else is the public debt. It's 70 percent of the total debt.

Current Status

On September 8, 2017, President Trump signed a bill increasing the debt ceiling to December 8, 2017.

Later that day, the debt exceeded $20 billion for the first time in U.S. history.

The bill also approved $15.25 billion in relief funds for the victims of Hurricane Harvey and Hurricane Irma. It included an extension of government spending to December 8 as well. Without a debt ceiling increase, the U.S. Treasury does not have enough to disburse the funds to FEMA. (Source: "Trump Signs Debt Limit Suspension Tied to $15 Billion Storm Aid," Bloomberg, September 8, 2017.)

On September 6, 2017, Trump and Congressional Democratic leaders agreed to raise the debt ceiling until mid-December. Senate Majority Leader Mitch McConnell, R-Ky., and House Speaker Paul Ryan, R-Wis., wanted to raise the ceiling without any restrictions. (Source: "Trump Agrees to Raise Debt Ceiling Until December," Politico, September 6, 2017.)

That means Congress must approve a new debt ceiling and create a new budget by December 8. That will create a situation like the 2012 fiscal cliff crisis. (Source: "Congress Must Raise Debt Ceiling While Approving Harvey Aid," CNN Money, September 3, 2017.)

The House Freedom Caucus was furious. It wanted to impose a $1.5 trillion restriction. That would be enough to get the government through the 2018 midterm election.

It also wanted guarantees that the administration would cut the debt before allowing a ceiling increase. These include spending cuts and an assurance that debt repayment is the highest priority. (Source: "GOP Clash Looms Over Raising Debt Ceiling," Politico, August 3, 2017. "Freedom Caucus Eyeing $1.5 Trillion Debt Ceiling Increase," Politico, June 13, 2017.)

Congress needed to raise the ceiling before October 3, 2017. Otherwise, the federal government would have defaulted on 25 percent of its bills for that month. Congress suspended the debt ceiling on November 2, 2015, when it passed the Bipartisan Budget Act of 2015, Pub. L. 114-74. It remained suspended until March 15, 2017. That means the Treasury Department cannot allow the statutory debt limit to go one penny higher than the $19.808 trillion it was on that day.

(Source: "The Debt Ceiling Deadline Has Passed," Zero Hedge, March 17, 2017.)

Since March 2017, the Treasury has been raiding federal pension funds to keep from issuing new debt. It will run out of these extraordinary measures in early September. It can use incoming tax receipts to stay afloat until the October 3 cutoff date.

Debt Ceiling 2015

On February 11, 2014, House Speaker John Boehner passed a bill to suspend the debt ceiling until March 15, 2015. The debt ceiling would automatically become the level of the debt at that point in time. The bill approved without any attachments, riders or insistence that Obamacare be defunded. He didn't have 218 Republican votes to do so. Instead, he passed it with 193 Democrats and 28 Republicans.

Tea party Republicans in the House called it a "...complete capitulation on the Speaker's part and demonstrates that he has lost the ability to lead the House of Representatives." They and Senator Ted Cruz were the only ones who thought the threat of a debt default was a useful tool to force the government to cut spending. But there weren't enough of them to wield this ax. (Source: "Boehner Says House to Pass Clean Debt Limit Hike," Fox News, February 22, 2014.)

On March 15, 2015, the nation reached the debt ceiling of $18.113 trillion. In response, the Treasury Secretary stopped issuing new debt. He took extraordinary measures to keep the debt from exceeding the limit. For example, he stopped payments to federal employee retirement funds. He also sold investments held by those funds. He kept the debt under the limit until Congress passed the Budget Act on November 15. (Source: “Report on Fund Operations and Status,” Department of the Treasury, January 29, 2016. "Meet the New Debt Ceiling," CNN Money, March 17, 2015.)

Debt Ceiling History

Congress created the debt ceiling in the Second Liberty Bond Act of 1917. It allowed the Treasury Department to issue Liberty bonds so the U.S. could finance its World War I military expenses. These longer-term bonds had lower interest payments than the short-term bills Treasury used before the Act. Congress now had the ability to control overall government spending for the first time. Before that, it had only issued authorization for specific debt, such as the Panama Canal or other short-term notes. (Source: “The Debt Limit: History and Recent Increases,” CRS Report for Congress, 2008.)

This is no longer necessary. In 1974, Congress created the budget process that allows it to control spending. That's why Congress usually raises the debt ceiling. When the budget process works smoothly, both houses of Congress and the President have already agreed on how much the government will spend. There's no need for a debt ceiling. It merely allows the government to borrow money to pay the bills it has already approved. (Source: "1974 Budget Control Act," University of California Berkeley.)

Elected officials have a lot of pressure to increase the annual U.S. budget deficit. Increases in the budget pushes the national debt higher and higher. That's because there is not much incentive for politicians to curb government spending. They get re-elected for creating programs that benefit their constituency and their donors. They also stay in office if they cut taxes. Deficit spending does, in general, create economic growth.

When the Debt Ceiling Matters

Congress must raise the debt ceiling so the United States doesn't default on its debt. That usually isn't a problem. In fact, during the last 10 years, Congress increased the debt ceiling 10 times. It raised it four times in 2008 and 2009 alone. If you look at the debt ceiling history, you'll see that Congress usually thinks nothing of raising it.

The debt ceiling only matters when the president and Congress can't agree on fiscal policy. That occurred in 1985, 1995-1996, 2002, 2003, 2011 and 2013. It's a last resort to get attention by the non-majority in Congress. They might have felt slighted by the budget process.

For example, in January, 2013, Congress threatened not to raise the debt ceiling to force the federal government to cut spending in the Fiscal Year 2013 budget. Its position was that one dollar of spending should be cut for every dollar the debt ceiling was raised. President Obama replied he would not negotiate since the debt was incurred to pay bills that Congress already approved. Fortunately, better-than-expected revenues meant the debt ceiling debate was postponed until the fall. (Source: “Debt Ceiling Postponed,” Atlanta Blackstar, January 23, 2013.)

On September 25, 2013, Lew first warned that the nation would reach the debt ceiling on October 17. Many Republicans said they would only raise the ceiling if funding for Obamacare were taken out of the FY 2014 budget. At first, it looked like Boehner would pass a debt ceiling override without them. He didn’t want Republicans to be blamed for another fiasco like the 2011 debt crisis. Then he changed his mind.

On October 1, 2013, the government to shut down because Congress hadn't approved the funding bill. The Senate wouldn't approve a bill that defunded Obamacare. The House wouldn't approve a bill that funded it. Boehner announced he wouldn't raise the debt ceiling unless Democrats agreed to negotiate cuts in mandatory programs, such as Medicare, Medicaid and Obamacare. President Obama wouldn't negotiate a budget until the House approved a funding bill and raised the debt ceiling. At the last minute, the Senate and House agreed upon a deal to reopen the government and raise the debt ceiling. For more, see Government Shutdown.

On October 17, 2013, Congress agreed to a deal that would let Treasury issue debt until February 7, 2014. If it hadn't, the United States would have defaulted on its debt for the first time in its history.

The debt ceiling and government spending can also become a concern if the debt to gross domestic product ratio gets too high. According to the International Monetary Fund, that level is 77 percent for developed countries. When debt to GDP ratio rises too high, debt owners become concerned that a country can't generate enough revenue to pay the debt back.

What Happens If the Debt Ceiling Isn't Raised?

As the debt approaches the ceiling, Treasury can stop issuing notes, and borrow from its retirement funds. These funds exclude Social Security and Medicare. It can withdraw around $800 billion it keeps at the Federal Reserve bank.

Once the debt ceiling is reached, Treasury cannot auction new notes. It must rely on incoming revenue to pay ongoing federal government expenses. That happened in 1996 when Treasury announced it could not send out Social Security checks. Competing federal regulations make it unclear how Treasury could decide which bills to pay and which to delay. Foreign owners would get concerned that they may not get paid. See What Is the U.S. Debt to China?

If Treasury did default on its interest payments, three things would happen. First, the federal government could no longer make its monthly payments. Employees would be furloughed and pension payments wouldn't go out. All those receiving Social Security, Medicare and Medicaid payments would go without. Federal buildings and services would close.

Second, the yields of Treasury notes sold on the secondary market would rise. That would create higher interest rates. This would increase the cost of doing business and buying a home. It would slow down economic growth.

Third, owners of U.S. Treasurys would dump their holdings. That would cause the dollar to plummet. The dollar’s drastic decline could eliminate its status as the world's reserve currency. The standard of living in America would decline. In this situation, the United States would find itself unable to repay its debt.

For all these reasons, Congress shouldn't monkey around with raising the debt ceiling. If members are concerned about government spending, they should get serious about adopting a more conservative fiscal policy long before the debt ceiling needs to be raised.

What Happens When the Debt Ceiling Is Raised?

Continuing to raise the debt ceiling is how America wound up with a $19 trillion debt. The debt ceiling has become a joke. It has become more like a speed limit sign that is never enforced. In the short-term, there are positive consequences to raising the debt ceiling. America continues to pay its bills. Consequently, it has avoided a total debt crisis.

The long-term consequences are severe. That's because the paper-thin debt ceiling is apparently the only restraint on out-of-control government spending. A 2017 survey found that 57 percent of Americans said Congress should not raise the debt ceiling. Only 20 percent said it should be raised. But they don't want their taxes raised or their services cut. (Source: "Morning Consult National Tracking Poll #170604, " Morning Consult/POLITICO, June 19, 2017.)

"Many people seem to want to cut down the forest but to keep the trees," according to Humphrey Taylor, Chairman of Pollster Harris Interactive. The majority of those interviewed don't want to see cuts to health care, Social Security and education. Health care and Social Security are two of the largest budget items. They do want to see cuts in foreign aid which is one of the smallest budget items. They also want to see cuts to overseas defense spending which is one of the largest budget areas. They are saying "Cut programs that send my tax dollars overseas, and keep programs that help me personally."

The debt ceiling is good in that it creates a crisis that focuses national attention on the debt. Raising it is a necessary consequence of management by crisis.

👺

Paris, Nov 23, 2016 (AFP)

Donald Trump's election in the United States and a surge in far-right groups in Europe have led to a fierce debate among historians and commentators about the parallels between the current decade and the 1930s.

Some believe that drawing a comparison with a catastrophic decade that culminated in World War II is alarmist, underlining that populist movements emerging now are fundamentally different.

Others warn that the political reaction visible across Western democracies stems from the same sense of anger and bitterness documented in the 1930s, warning that the lessons of history should not be ignored.

Here are 10 quotes from leading commentators on the subject:

"It will be as exciting as the 1930s, greater than the (president Ronald) Reagan revolution -- conservatives, plus populists, in an economic nationalist movement."

- President-elect Donald Trump's chief strategist Steve Bannon in an interview with The Hollywood Reporter, November 19

"Modern populism lacks the level of violence and the anti-democratic character it had in the 1930s."

- British historian Richard Overy, author of "The Morbid Age", to AFP, November 17

"I never really understood how fascism could have come to Europe, but I think I understand better now."

- New York Times editorialist David Brooks in a column entitled "Are We On The Path To National Ruin?", July 12.

"A look at the polls in Austria and Germany -- Austria and Germany -- cannot fail to evoke unpleasant memories for those familiar with the 1930s, even more so for those who watched directly, as I did as a child."

- American political theorist and historian Noam Chomsky, talking to the truth-out.org website, November 14.

"We are not in the 1930s. We are not being crushed between the monolithic alternatives of fascism and communism."

- Antony Beevor in an article called "This is no rerun of the Thirties -- but the world is changing at terrifying pace", The Daily Telegraph, November 11.

"We are starting to understand since Trump that it is not just the wild dream of a few intellectuals saying 'watch out, fascism is coming back'."

- French historian Pascal Blanchard, author of "The 1930s are back: A little history lesson to understand the current crisis", to AFP, November 16

"The populism is different to the 1930s but of course it has echoes of it."

- Ian Kershaw, author of "To Hell and Back", a history of Europe from 1914-49, to AFP, October 15.

"Comparisons with the 1930s are fatuous... Nonetheless, it is clear that an exclusive, often ethnically-based, form of nationalism is on the march."

- The Economist article on nationalism, November 19

"Democracy often brings fascists to power, it did so to Germany in the 1930s."

- British historian Simon Schama, November 9, BBC radio

"In the work of preserving civilisation, nine-tenths of the job is to understand the past and stress its most obvious lessons. Now would be a good time to re-remember the 30s."

- Pulitzer-winning columnist Brett Stevens in a piece titled "The Return of the 1930s", The Wall Street Journal, March 7

adp/gj/hmw

<org idsrc="isin" value="US6501111073">THE NEW YORK TIMES COMPANY</org>

😬

news.com.au: DONALD Trump has long cultivated an aura of unadulterated success, but those who scratch beneath the surface find a different story.

While the former reality television star is adept at captivating an audience, he has left a string of failures behind him, including six bankrupt businesses.

Economists are afraid he could do the same to the US economy — and there would be no coming back.

The President-elect campaigned on a platform of cutting taxes and increasing spending, and no one is quite sure where the savings would come from.

It could leave America buried under an even greater mountain of debt by the time his four-year term is over.

One of the first things Mr Trump plans to do after his inauguration in January is lower the corporate tax cap from 35 per cent to 15 per cent. In the short-term, this is likely to be a good thing, according to Tom Switzer from the US Studies Centre.

“Given the Republicans have control of the House of Representatives and the Senate, it’s more likely to pass and stimulate the economy,” Mr Switzer told news.com.au.

“That’s probably why Wall Street rallied [following the initial hit to the market after Mr Trump’s election]. He’s shown that, at least in the short-term, he’s pro-growth.

“But where’s he going to get the money for tax cuts and to increase spending, notably on infrastructure? He may face more deficit problems in four years.”

GAME OF RISK

In 1991, the Trump Taj Mahal in Atlantic City was nearly $US3 billion in debt when it filed for bankruptcy, and Mr Trump gave up half his stake in the casino and selling his yacht and airline.

A year later, the Trump Plaza Hotel in New York filed for bankruptcy while $US550 million in debt, with the real estate mogul giving up a 49 per cent share but remained a figurehead CEO. Another casino, Trump Castle, also went bankrupt along with the Trump Plaza Hotel and Casino in Atlantic City, which was $US250 million in debt.

In 2004, Trump Hotels and Casinos Resorts, which includes the Taj Mahal, Trump Marina and Trump Plaza casinos in Atlantic City, filed for bankruptcy with an estimated $US1.8 billion in debt. The President-elect reduced his share in the company from 47 to 27 per cent and it was renamed Trump Entertainment Resorts, before it again went bankrupt in 2009 after a missed $US53.1 million bond interest payment during the global financial crisis. Mr Trump resigned as chairman and reduced his stake to 10 per cent.

Early this month the Trump International Hotel & Tower Toronto went bust, just four years after Mr Trump and his children cut the ribbon at its opening. He is not the developer or even an investor, but was paid for his name and management team.

As he and his children said in a CBS 60 Minutes interview on Monday, none of that matters any more. Some believe his bid for the presidency is simply his latest hubristic plan to gild his name and image.

TRILLIONS IN DEBT

Global markets were thrown into disarray after the election result was announced, but recovered surprisingly quickly following Mr Trump’s conciliatory victory speech.

Traders around the world will be waiting to see whether the new president will carry out the campaign promises economists estimated would increase national debt by trillions of dollars.

Not only has he promised corporate tax cuts, he wants to reduce the top income tax bracket from 40 per cent to 33 per cent. The President-elect claimed the cuts will pay for themselves by eliminating some deductions and credits, but both left-of-centre Tax Policy Center and the right-of-centre Tax Foundation say this is nowhere near true, and the scheme would cost $US9 trillion in revenue over the first decade. The question, then, is where he will find the money to carry out his plan to both cut tax and raise government spending.

The Wall Street Journal’s economics blog reported that he would make savings with large tax cuts from repealing Barack Obama’s signature Affordable Care Act and slashing discretionary spending, but has promised far greater increases in spending on defence, veterans’ programs and childcare.

THE WHEELER AND DEALER PRESIDENT

The United States’ debt already stands at 75 per cent of gross domestic product. The only “advanced economies” with higher debt are Italy, Japan, and Portugal, according to the International Monetary Fund.

History has already shown us what happens when a president follows such a strategy, according to Daniel Altman, an adjunct associate professor of economics at New York University’s Stern School of Business, writing in Foreign Policy.

Ronald Reagan and George W. Bush both spent heavily on the military while drastically cutting income tax, each leaving the nation in such great debt their successors were forced to raise taxes back up again.

But Mr Trump’s greatest hurdle could come from within his own party. “There is fear in the global markets, the global economy is showing signs of contraction and there could be a recession,” said Switzer. “Republicans could disagree more with Trump on spending than the Democrats.

“He changed political parties five times. He’s an erratic character, he’s not bound by ideology. He’s a pragmatic wheeler and dealer, he could be very loose with the strings.”

If Mr Trump and Congress do approve big cuts and spending to drive growth, it could lead to the debt becoming unsustainable, causing a “deficit crisis”, says Switzer.

“The Federal Reserve will likely put the brake on Trump via interest rates,” he said.

But the Treasury has already refinanced the nation’s debt at low interest rates so there are limits to what it can do, Altman writes in Foreign Policy. “If he stays true to his record in business, another bankruptcy could be on the horizon.”

The question is whether the billionaire businessman would stick around to watch his greatest vanity project implode.

👀

Donald Trump’s movement has often been compared to that of a rightwing European party. Now, his union with Europe’s right is official. At a rally on Wednesday Trump presented himself as America’s Nigel Farage, holding the former Ukip leader up as his populist, nationalist twin.

Make it a long-lost twin for Trump, who when first asked for an opinion on whether Britain should leave the European Union appeared to be unfamiliar with the referendum in question. Fast-forward to the day after the referendum, though, and Trump would boast he had predicted the British exit from the EU all along. Earlier this month he rebranded himself “Mr Brexit” in a tweet; and now he’s getting even more explicit about what promise he sees in the tale of British secession.

“On 23 June, the people of Britain voted to declare their independence – which is what we’re looking to do also, folks! – from international government,” Trump told his audience in Jackson, Mississippi.

Jackson is a place where the memory of the Confederacy is still fresh, and as such a curious one in which to be touting a second independence day, of sorts. But such white nationalist fervour seemed to play well with the overwhelmingly white crowd assembled in the largely black city on Wednesday night.

The architects of Brexit like to frame the vote as a righteous backlash against powerful elites. As Farage put it on Wednesday: “You can beat the pollsters. You can beat the commentators … Anything is possible if enough decent people are prepared to stand up against the establishment.”

According to this oft trotted-out framing, Trump’s reviled Washington establishment is a parallel for Farage’s European Commission. But the hyper-focus on anti-elitism obscures the far less righteous xenophobia, racism and anti-immigrant sentiment that were also elements of the leave campaign.

Such uninspiring qualities are the core of Trump’s movement too, and that was apparent in no small number of crowd-pleasing lines. “Why do our leaders spend so much more time talking about how to help people [who are] here illegally than they spend trying to help American citizens?” Trump asked. “The media ignores the plight of Americans who have lost their children to illegal immigrants, but spends day after day pushing for amnesty for those here in violation of the law.”

The bigotry of Trump’s campaign is, if anything, more extreme. While leave campaign leaders such as Boris Johnson would at least distance themselves from the anti-immigrant rhetoric espoused by Farage and others, Trump has embraced it. And even Farage himself has suggested that some of Trump’s anti-Muslim rhetoric goes too far.

Trump has long harnessed America’s wave of white nationalism. But with the encouragement of his campaign’s new chief executive, Stephen Bannon(previously an outspoken Brexit cheerleader at the rightwing Breitbart news website), he has now harnessed something else. Namely, he’s enlisted Farage to help him airbrush bigotry from his message in much the same way Farage did with Brexit.

It’s telling that in the wake of Brexit’s victory Farage has, rather than assuming a position of leadership, found himself stoking populist flames elsewhere. And it underscores another unspoken parallel with Trump: trafficking in the politics of anger – not governance – is what he does best. If Trump wins in November, expect more of the same.

👀

Meski Bank Sentral Amerika Serikat (the Fed) belum menurunkan maupun menaikkan suku bunga acuannya, namun pemerintah Indonesia telah menyiapkan beberapa upaya antisipatif agar perekonomian Indonesia tetap berada pada jalur positif.

Hal tersebut diungkapkan oleh Menteri Keuangan (Menkeu) Sri Mulyani di Kantor Kementerian Koordinator Bidang Perekonomian, Jakarta, Selasa (8/11/2016).

Sri Mulyani mengatakan, pada prinsipnya pemerintah memandang ketidakpastian yang berasal dari luar negeri telah diantisipasi dengan pengelolaan perekonomian nasional.

"Tentu kita pasti dari sisi pengelolaan perekonomian akan melihat semua sektor dari sisi sumber-sumber ekonomi, apakah ini akan mempengaruhi sisi ekspor impor, dan itu juga akan mempengaruhi kepada nilai tukar," kata dia.

Tidak hanya itu, mantan Direktur Bank Dunia ini menyebutkan, pemerintah akan menetralisir dan memperkuat sumber-sumber perekonomian nasional. Sedangkan dari sektor keuangan atau perbankan, Sri Mulyani meyakini regulator dalam hal ini Bank Indonesia dan Otoritas Jasa Keuangan (OJK) telah berkoordinasi untuk melihat kemampuan ekonomi nasional dari neraca jikalau terjadi sentimen dari luar negeri.

"Dari sisi ekonomi riil, ekonomi Indonesia kemarin pertumbuhan ekonominya relatif cukup baik, yang dianggap titik-titik untuk diperbaiki belanja pemerintah, karena kuartal 3 dilakukan penyesuaian pada APBN, tapi itu secara seasonal, tapi pada kuartal IV akan ternetralisir," tambahnya.

Upaya yang dilakukan pemerintah untuk menjaga perekonomian dari sentimen negatif luar negeri juga akan disisir dari sektor ekspor dan impor. Menurut Sri Mulyani, dua sektor tersebut masih relatif baik sekaligus mampu menetralisir dampak yang ditimbulkan dari kebijakan Bank Sentral AS.

"Dari sisi lainnya perdagangan kita punya cadangan walaupun ekspornya negatif tapi kita masih bisa masih dikompensasi dari PMA, maupun yang mereka masuk melalui Surat berharga negara, itu bisa mengurangi sentimen negatif," tandasnya.

Supercharging the bluster, hyperbole and media mastery that made him one of the world's best-known businessmen, Donald Trump upended U.S. democratic traditions on a 17-month quest he hopes will lead to the White House.

From his grand Trump Tower escalator entrance into the Republican presidential race on June 16, 2015, Trump managed to be simultaneously charismatic and combative, elitist and populist, lewd and pious as he drilled into a lode of polarity and anti-Washington anger among American voters.

In Tuesday's election against Democrat Hillary Clinton, Trump is making his first run for public office. Trump called it a movement, not a campaign.

He drew enthusiastic crowds to rallies where people cheered him for "just saying what everybody's thinking." Critics labeled him misogynistic, ill-informed, uncouth, unpresidential, a racist, a hypocrite, a demagogue and a sexual predator, all accusations he denied.

It took Trump, 70, little more than 10 months to vanquish 16 other candidates and become the first major party nominee since General Dwight Eisenhower in the 1950s to have no government experience. He drew a record number of votes in primary contests but in so doing created a rift in the party.

Then he squared off against Clinton, 69, in a race marked by controversies that included upheaval in his staff, charges he had groped women, and his claim, never supported, that Clinton and the media had rigged the election against him.

He shocked many by saying he might not accept the election result if he lost, repudiating a U.S. tradition of peaceful government transition. He said that as president he would investigate Clinton for her use of email while secretary of state. He vowed to send her to jail.

His campaign took a scandalous turn in October with the release of a 2005 video in which Trump, unaware he was being recorded, told a television entertainment reporter that he liked to kiss women without invitation and that, because he was rich and famous, he could "grab them" by the genitals without recriminations.

Trump dismissed the remarks as "locker room talk" and denied the subsequent accusations from more than 10 women who said he had groped them or made unwanted sexual advances.

GLOOM OVER AMERICA

Throughout his campaign - and especially in his Republican convention speech in July - Trump described a dark America that had been knocked to its knees by China, Mexico, Russia and Islamic State. The American dream was dead, he said, smothered by malevolent business interests and corrupt politicians, and he said he alone could revive it.

Trump said he would make America great again through the force of his personality, negotiating skill and business acumen. He offered vague plans to win economic concessions from China, to build a wall on the southern U.S. border to keep out undocumented immigrants and to make Mexico pay for it. He vowed to repeal Obamacare while being the "greatest jobs president that God ever created" and has proposed refusing entry to the United States of people from war-torn Middle Eastern nations, a modified version of an earlier proposed ban on Muslims.

Trump promoted himself as the ultimate success story. He dated beautiful women, married three of them, had his own television reality show and erected skyscrapers that bore his name in big gold letters. Everything in his life was the greatest, the hugest, the classiest, the most successful, he said, even though critics assailed his experiences with bankruptcies, the failures of his Atlantic City, New Jersey, casinos and what they viewed as the misplaced pride he showed when presented with evidence he avoided paying taxes.

Trump had flirted with presidential runs in the past and some initially saw his campaign as a vanity project meant to indulge his ego and burnish his brand. It was expected to be short-lived but as the election season progressed, he became the front-runner, winning state nominating contests despite an unconventional campaign that relied on large-scale rallies and mostly ignored grass-roots work.

His hired advisers came to realize there was only so much they could do to rein him in. His inner circle was dominated by his three oldest children - Donald Jr., Eric and Ivanka, along with Ivanka's husband, Jared Kushner.

TWEET ATTACKS

The rise of Trump, once a registered Democrat, threatened to blow up the Republican Party. Its establishment challenged his commitment to their tenets and organized against him. Prominent Republicans - including former presidents George H.W. Bush and George W. Bush and congressional leaders - shunned him or offered lukewarm support.

Trump used Twitter as a weapon, firing off insults and mockery at those who offended him, including "Crooked Hillary" and Republican rivals "Little Marco" Rubio, Jeb "Low Energy" Bush and "Lyin' Ted" Cruz.

Another target was the family of a Muslim U.S. Army captain who died fighting in Iraq after the soldier's father had spoken against Trump at the Democratic National Convention. Trump sniped back for days despite advice to move on.

As of late October, the New York Times had counted 282 people and things he had insulted on Twitter since declaring his candidacy.

The Trump candidacy was brimming with contradictions. The candidate who vowed to bring back jobs to the United States had his clothing line and campaign hats manufactured in foreign countries. The man who decried the corrupting power of money in politics boasted of having bought influence himself.

Undocumented workers had been used on his building projects but as a candidate Trump vowed to ship illegal immigrants out of the country. He said no one respected women more than he did but even before the groping accusations emerged, he was branded a misogynist for making fun of the appearance of rival candidate Carly Fiorina and an apparent reference to the menstrual cycle of Fox News' Megyn Kelly.

"YOU'RE FIRED!"

Trump's campaign trail demeanor seemed to draw from his experiences as host of "The Apprentice," a reality TV show where he barked a crowd-pleasing "You're fired!" at contestants who fell short in competitions.

His speeches were often unscripted and featured boasts on everything from his money to his IQ. He peppered them with dubiously sourced declarations, misperceptions and false statements.

He suggested that gun rights activists could act to stop Clinton from nominating liberal U.S. Supreme Court justices, a remark the Clinton campaign called dangerous.

Trump boasted of a fortune he put at $10 billion, although in September Forbes magazine estimated it at $3.7 billion, making him the 156th richest American.

Trump regularly made comments that would have doomed a more conventional candidate, such as when he said his supporters were so loyal that he could shoot someone on 5th Avenue in New York and not lose a single vote.

In May he would draw accusations of racism for questioning the impartiality of a judge - born in the United States to Mexican immigrants - who was hearing a lawsuit against him.

No other candidate referred to the size of his genitals during a debate. He was flattered when Russian President Vladimir Putin called him a “brilliant and talented leader.”

Trump mocked Senator John McCain, the Republicans’ presidential candidate in 2008, for having been captured during the Vietnam War and said he wanted to punch a protester in the face at a Trump rally.

DIFFICULT CHILD

Trump was born to money on June 14, 1946, in the New York City borough of Queens, the fourth of five children of Fred Trump, who would become one of the city's biggest developers and landlords, and his wife. It was Fred Trump who taught Donald the value of self-promotion and a killer instinct.

By his own admission, Trump was not an easy child and in the eighth grade his parents sent him to the New York Military Academy in hopes of instilling needed discipline. Through student and medical deferments during the Vietnam War, Trump would never serve in the U.S. military but said the school gave him "more training militarily than a lot of the guys that go into the military."

After graduating from the University of Pennsylvania, Trump went to work for his father's company, which focused on the outer New York City boroughs of Queens, Brooklyn and Staten Island and owned an estimated 15,000 apartments. In 1973 the Trumps were charged with racial bias in their rental practices before reaching a settlement with the U.S. government.

With a $1 million loan from his father, Trump eventually went into business himself in Manhattan, where he became a regular at some of the city's most exclusive clubs and developed a reputation as a ladies' man.

TRUMP TOWER FLAGSHIP

He soon made his mark with a series of real estate and development deals, including redoing an old hotel at New York's Grand Central Terminal. In 1983 he opened his flagship, 58-story Trump Tower, which serves as both his primary residence and Trump Organization headquarters.

More projects around the world would follow, including golf courses, the Mar-a-Lago private resort in Florida, New York's venerable Plaza Hotel and casinos.

Trump's projects had mixed success. The flops included the real estate-oriented Trump University, Trump Mortgage, Trump Airlines and Trump Vodka but it was his experience with four casinos in Atlantic City, New Jersey, that took the golden luster off his empire.

Timothy O'Brien, author of "TrumpNation: The Art of Being the Donald," wrote that in the 1990s Trump was out of money and twice had to go to his siblings for loans. A former employee said the Trump Organization would have shut down if the family had not come through but Trump disputed that in his 1997 book "Trump: The Art of the Comeback."

While he never filed for personal bankruptcy, the downturn in the gaming industry sent parts of Trump's corporate empire to bankruptcy court in 1991, 1992, 2004 and 2009. In the 2009 bankruptcy, the unsecured creditors received less than a penny on the dollar for their claim. Trump resigned as chairman four days before the filing.

(Writing and reporting by Bill Trott in Washington; Additional reporting by Diane Craft; Editing by Howard Goller)

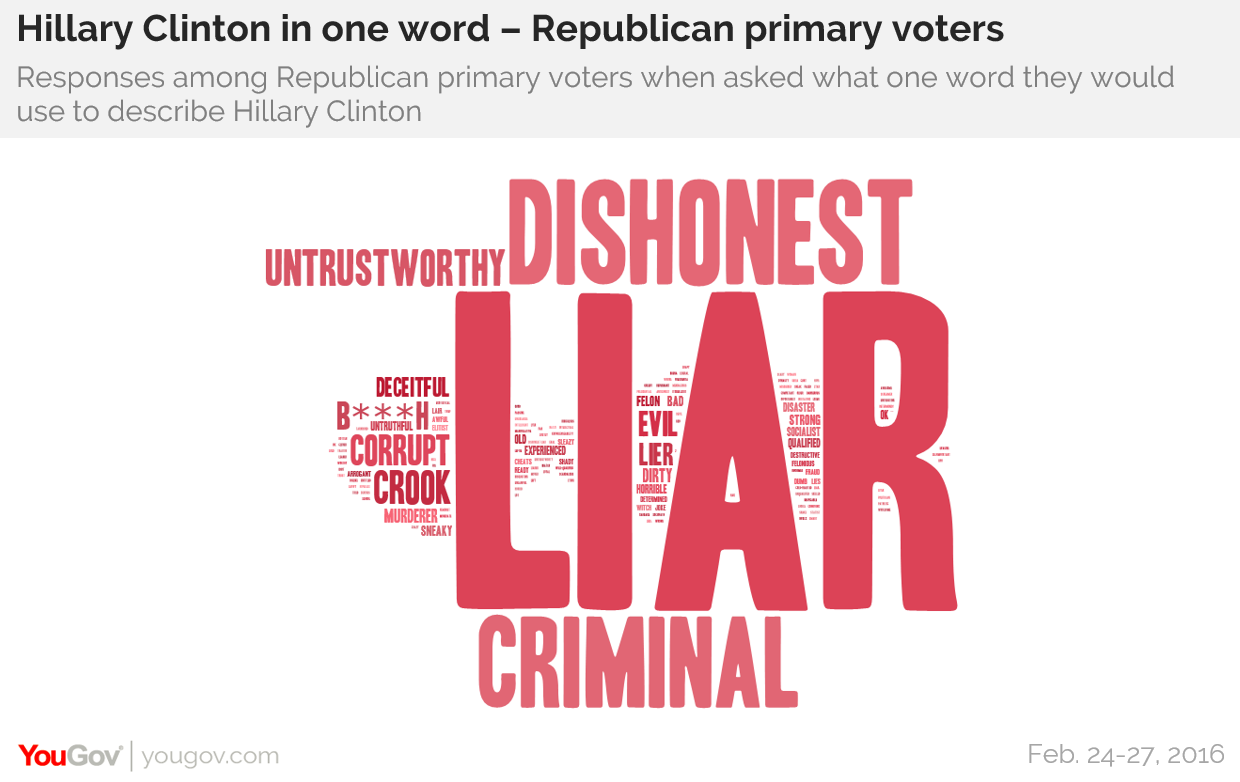

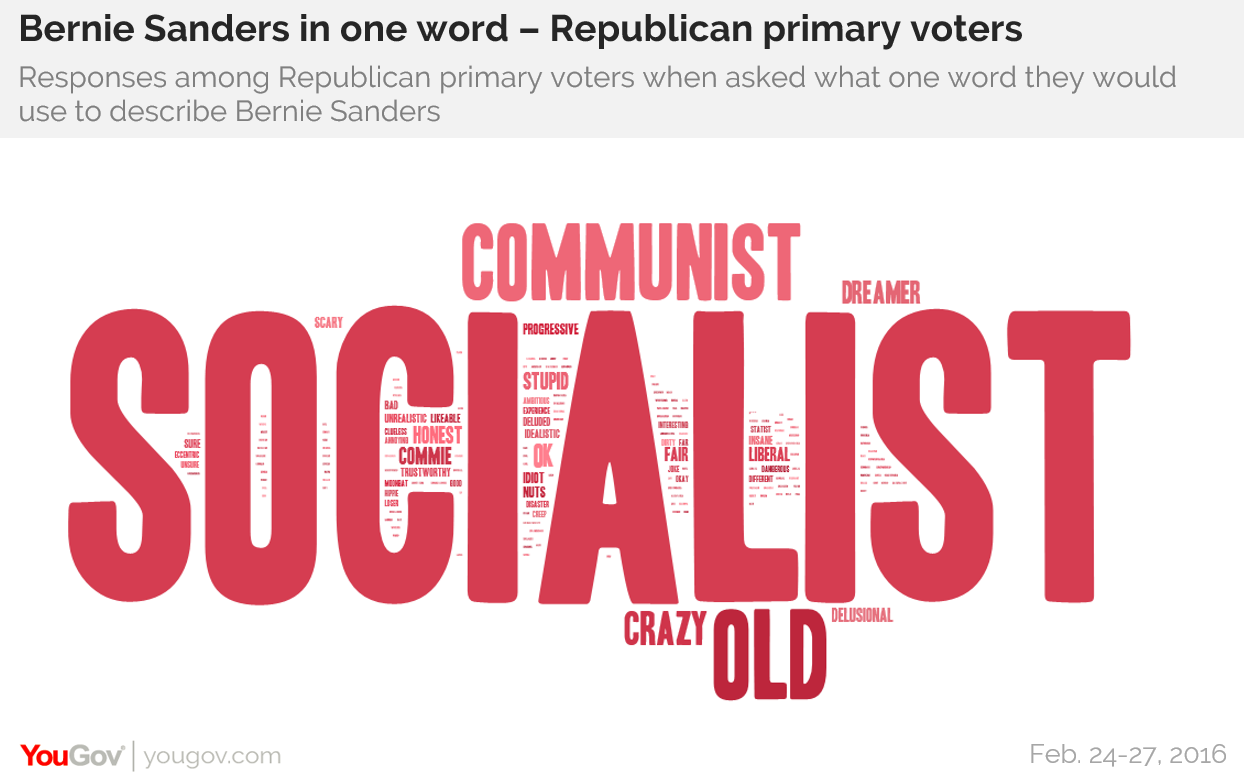

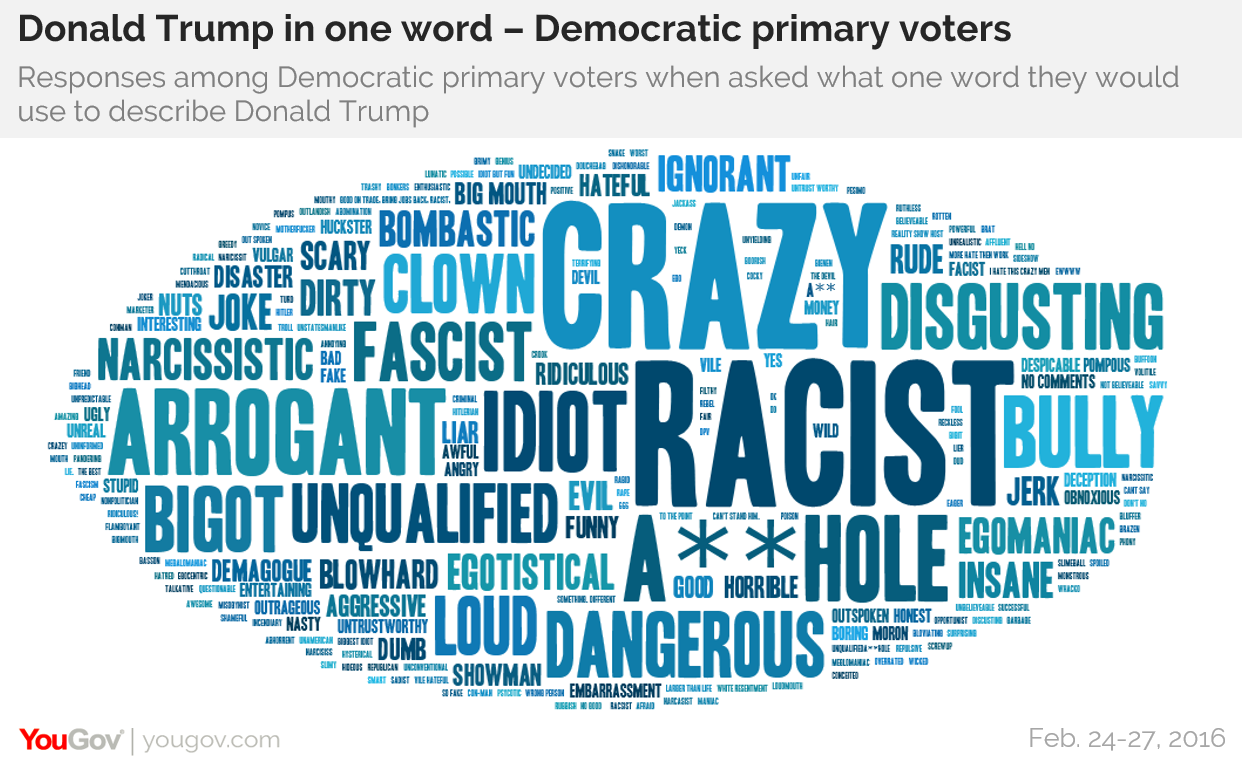

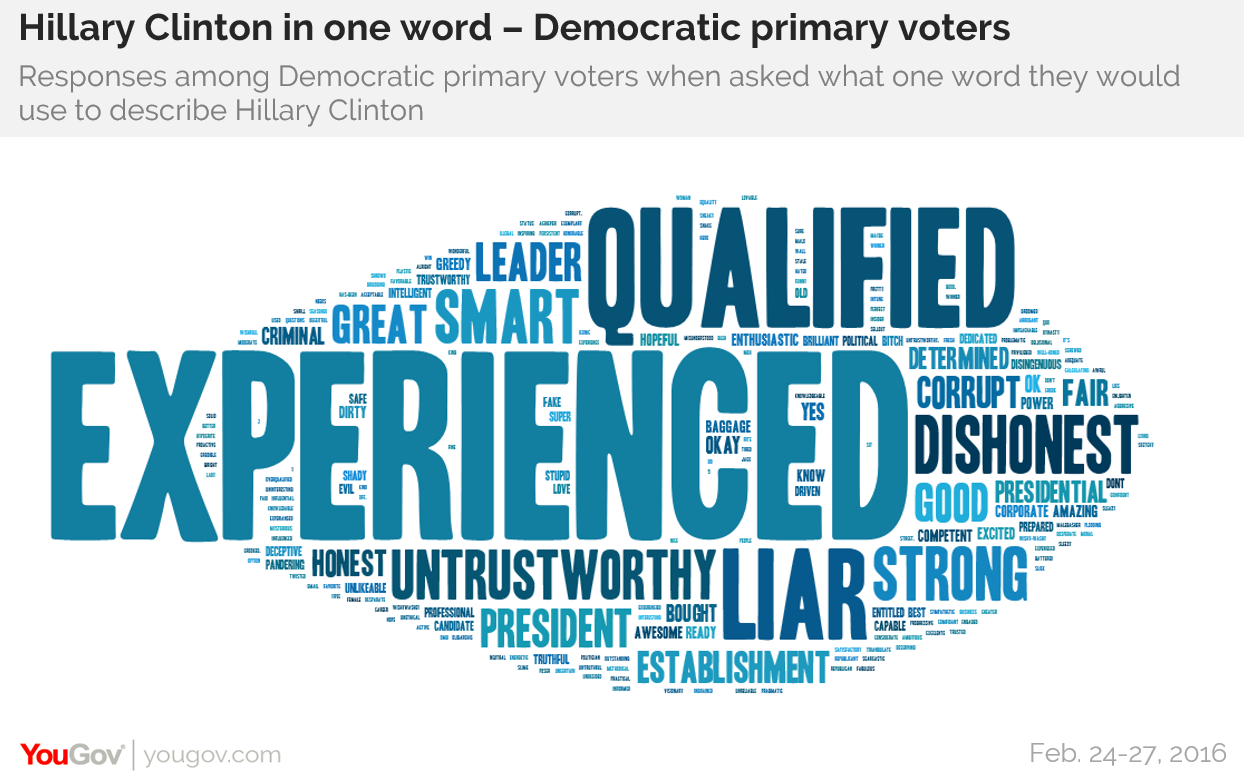

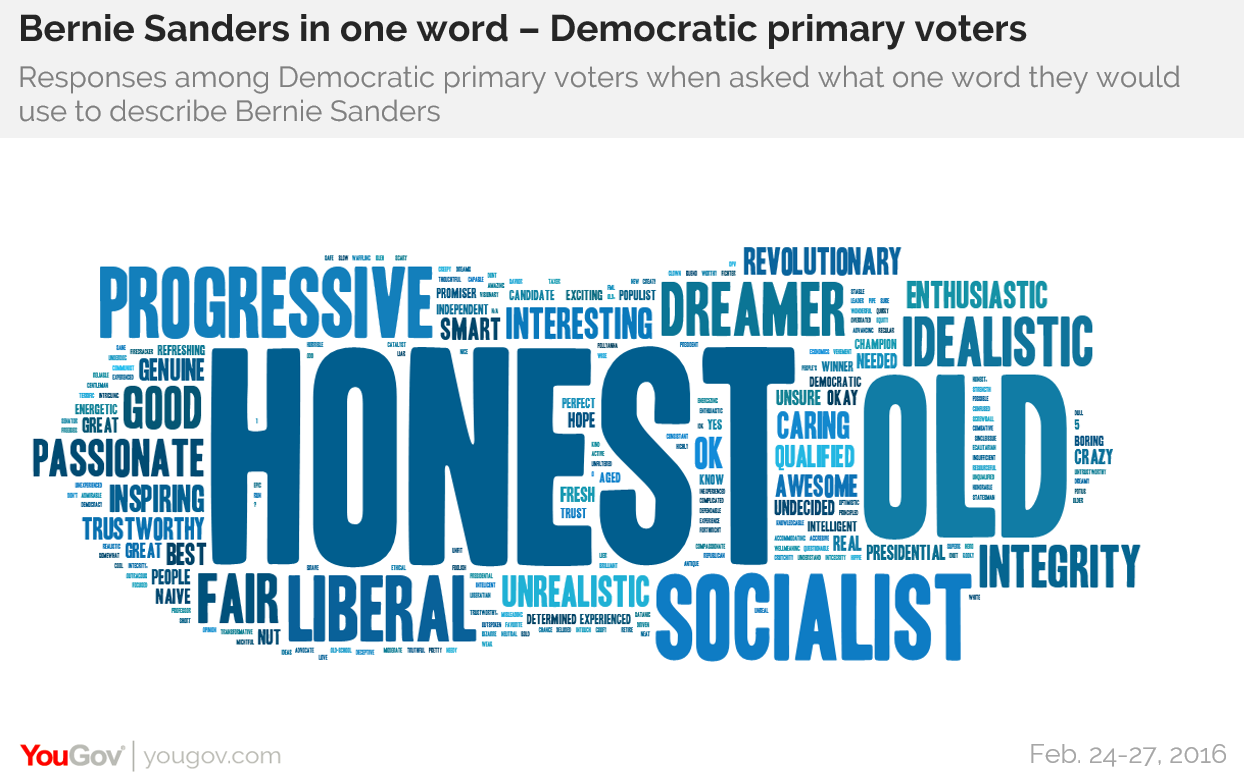

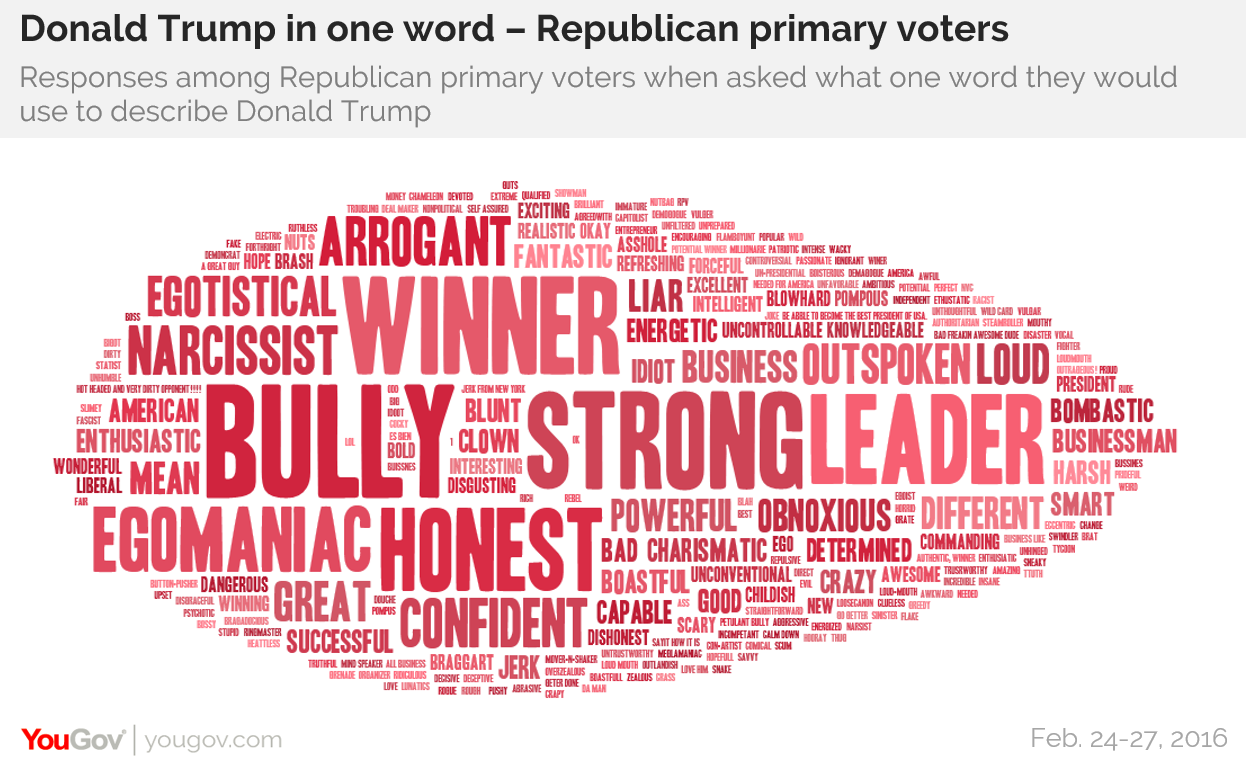

"Crazy" vs. "Dishonest"? Candidate images from both sides

YouGov asked Republican and Democratic voters to describe the presidential candidates in one word

Follow @YouGovUS on twitter and stay up to date with the latest news and results

The images of several leading presidential candidates this year seem set in stone, at least among those in the other political party. Those negative assessments – held by voters in the other party – are clear and perhaps unalterable. In the latest Economist/YouGov Poll (conducted just before Super Tuesday), voters were asked to give a one-word assessment of the remaining candidates running for president.

The negatives are obvious – many voters don’t trust former Secretary of State Hillary Clinton, Vermont Senator Bernie Sanders is seen as a socialist, and Republican frontrunner Donald Trump, praised by many for “telling it like it is,” is also rebuked by many for his behavior.

The vast majority of Republican primary voters see Clinton exactly the same way – calling her a “liar.”

As seen in the word cloud, if a Republican primary voters didn’t use the world “liar” to describe Clinton, nearly all used words that mean the same thing.

That reflects other findings in the poll and recent campaign discussion. Only 9% of Republican voters had a favorable opinion of Clinton, and only 5% said she was honest and trustworthy. Former GOP nominee Mitt Romney, in a speech denouncing Trump this week, said that “A person so untrustworthy and dishonest as Hillary Clinton must not become president.” In that same speech, Romney called Trump a “con man and a fake.”

Given that extreme dislike for Clinton as a person, it may not be a surprise that given the choice, three times as many Republican primary voters favored Sanders over Clinton for the nomination in that poll (though half didn’t favor either). But Sanders has the quality Republican voters think Clinton lacks: the perception of honesty. Nearly half of GOP voters regard Sanders as honest and trustworthy. And while 73% would be “upset” if Clinton won the nomination, less than half would be “upset” if Sanders did.

However, most Republican voters still don’t like Sanders. He has his own negative – and it is ideological. Just as nearly all the bad things Republican voters say about Clinton focus on honesty, the words that Republican primary voters use for Sanders are “socialist” and even “communist.” Even though he is the oldest candidate in the field (Sanders is 74 years old), just a small number say “old.”

Lindsay Graham, who left the GOP presidential race last year, said in a January radio interview that “dishonesty beats crazy,” and that may summarize how opponents view the two party’s frontrunners. Graham’s full quote is: “Dishonest — which is Hillary Clinton in the eyes of the American people — beats crazy,” he said. “I think Donald Trump’s domestic and foreign policy is gibberish.”

Democratic primary voters seem to agree with Graham’s characterization. They also have reacted to the variety of Trump statements attacking Mexicans, Muslims and the confusion over whether or not he would accept an endorsement from a leader of the Ku Klux Klan.

While a little of their opponents’ negative characterizations shows up in the words a candidate’s own partisans use to describe them, positive assessments dominate, as each of these three get highly favorable assessments from their own party’s voters. Clinton is seen as qualified and experienced, Sanders as honest, and Trump as strong and a winner.

the street: Editor's note: This story was originally published in October. As Republican presidential nominee Donald Trump will appear in a town hall in New York tonight, it's worth taking another look at what the U.S. economy may look like under a President Trump. Also, check out our Donald Trump Stock Portfolio, which we'll be tracking until November 8. The sections below on immigration, taxes and trade have been updated.

There's no denying Trump has done a good job of making himself rich -- he's worth somewhere between $4.5 billion and $10 billion, depending who you ask. Can he make the rest of America rich, too?

The economy isn't something Trump looks forward to tackling. In a January interview with "Good Morning America," Trump offered up a bleak assessment of the U.S. economy but added that, in terms of fixing it, it's a task he'd rather skip.

"We're in a bubble," he said. "And, frankly, if there's going to be a bubble popping, I hope they pop before I become president because I don't want to inherit all this stuff. I'd rather it be the day before rather than the day after, I will tell you that."

In an April interview with the Washington Post, Trump reiterated his doomsday view of the economy, suggesting we might be headed for recession. But this time around, he appeared more open to the idea of his being in charge of finding remedies. "I can fix it. I can fix it pretty quickly," he said. And most recently, he maligned the Federal Reserve for creating what he says is a "false economy."

Many Americans appear to believe that is the case and that, more broadly, a Trump presidency would be good for the economy. According to a March CNBC All-America Survey, Americans rate Trump and Democratic frontrunner Hillary Clinton evenly on key economic issues. And a recent CNN/ORC poll shows Trump rating higher than Clinton on the economy among voters.

Trump has certainly been this election cycle's most riveting figure. He initially focused his attention on immigration reform, calling for a wall to be built between Mexico and the United States and demanding the deportation of 11 million undocumented immigrants. He has wavered on that last point as of late.

Trump has made plenty of enemies along the way as well, including but limited to fellow GOP contenders Ted Cruz and Jeb Bush, New York Mayor Bill de Blasio, Fox News journalist Megyn Kelly, the media in general and even the Pope.

Those who fear Trump's plans should find common cause with those who love them: "I'm not sure how much of what he actually says today will be his positions a year from now," said Michael Busler, professor of finance at Stockton University.

Trump's own campaign has suggested he is playing "a part" to garner votes.

While Trump certainly has some grandiose ideas -- and equally lofty rhetoric to accompany them -- deciphering the exact nature of his economic policies is a complex task, according to John Hudak, a fellow in governance studies at Washington, D.C.-based think tank the Brookings Institution.

Not to mention the fact that if he does make it to the Oval Office, Trump won't have a free pass from Congress, even if it remains under the control of the Republican Party (as you'll see, many of his positions don't exactly hew closely to GOP policies).

Taking legislative hurdles out of the equation, what will the U.S. economy and markets look like if Trump becomes No. 45.

The American Action Forum, a right-leaning policy institute based in Washington D.C., estimates that immediately and fully enforcing current immigration law, as Trump has suggested, would cost the federal government from $400 billion to $600 billion. It would shrink the labor force by 11 million workers, reduce the real GDP by $1.6 trillion and take 20 years to complete (Trump has said he could do it in 18 months).

"It will harm the U.S. economy," said Doug Holtz-Eakin, president of the American Action Forum and chief economic policy adviser to Sen. John McCain's 2008 presidential campaign. "Immigration is an enormous source of economic vitality."

The impact would be felt on both supply and demand.

A number of industries that depend heavily on cheap immigrant labor would be devastated -- especially agriculture. "There would be an abrupt drop in farm income and a sharp rise in food prices," said John McLaren, professor of economics at the University of Virginia with expertise in international trade, economic development and the political economy.

Companies that sell to the immigrant population would be affected as well, leading to decreased revenues for local businesses and a loss of American jobs.

"Immigrants, whether they are legal or illegal, always spend a portion of their earnings in the location where they have their jobs," McLaren said. "And in a lot of our urban centers, this is actually an important part of the economy."

He pointed to the case of Postville, Iowa, where in 2008 U.S. Immigration and Customs Enforcement (ICE) raided a slaughterhouse and meat packing plant, detaining 389 undocumented workers (and jailing 300 of them). The raid caused most of the more than 1,000 immigrants not caught to leave the town of 2,300, devastating the local economy in the process.

He also noted his own research, which suggests each immigrant creates 1.2 local jobs for local workers, most of which go to U.S. natives. "Obviously, those jobs would disappear if the undocumented were just yanked away," he said.

It is worth noting that Trump appears to have backed away from his mass deportation stance slightly as of late, outlining priorities that would lead to the deportation of what The Washington Post estimates would be 5 million to 6.5 million immigrants. He has warned, however, that "anyone who has entered the United States illegally is subject to deportation."

Trump has also discussed reducing the number of jobs held by legal immigrants, namely by increasing the prevailing wage requirements for H-1B visas (visas that allow U.S. employers to recruit and employ foreign professionals) -- an element of his plan that is often overlooked. The Republican contender's thesis is that doing so would force companies to give jobs to domestic employees instead of overseas workers. The maneuver would benefit some, but not most.

"If I'm an American software programmer, I probably would benefit somewhat from making it harder for highly-skilled software programmers from elsewhere," McClaren said. "It's really hard to argue that the country, as a whole, benefits from that. It would be bad for most Americans, and it certainly would be bad for corporations."

An extreme anti-immigration policy could also cause collateral damage to the American image. "What's the American brand after we've rounded up 11 million people and sent them packing?" said Jim Pethokoukis, a columnist and blogger at the American Enterprise Institute, a center-right think tank based on Washington, D.C. "Do people still view America the same way?"

Trump's tax plan, unveiled in September, is perhaps the most detailed proposal he has put forth yet. It essentially entails implementing tax cuts across the board and literally sets forth a scenario in which the lowest earners get to send a form to the IRS reading, "I win."

"His tax plan is one of the most dynamic and pro-growth tax plans out there," said Merrill Matthews, resident scholar at the Institute for Policy Innovation, a Texas-based, right-leaning think tank. "You would find a huge amount of new business investment and companies willing to put their money out there to begin growing the economy."

Trump's tax plan stacks up fairly well against his fellow Republican presidential contenders. It isn't as drastic as proposals put forth by Ted Cruz and Ben Carson but does, like most GOP tax structures, favor the rich. Perhaps the biggest distinguishing feature of Trump's proposal is his hard cap on business taxes at 15%, which might be especially appealing to freelancers and the self-employed.

But there's a catch: Trump's tax plan would reduce revenue enormously, and the federal budget deficit would almost inevitably skyrocket.

Nonpartisan tax research group the Tax Foundation calculates that Trump's plan would cut taxes by $11.98 trillion over the course of a decade. It would lead to 11% growth in the GDP, 6.5% higher wages and 29% larger capital stock as well as 5.3 million jobs. However, it would also reduce tax revenues by $10.14 trillion, even when accounting for economic growth from increases in the supply of labor and capital.

"That tax cut would produce faster economic growth and a bigger economy -- as long as you pay zero attention to the fact that it would dramatically increase the deficit and budget debt," said Pethokoukis.